Health Transformation in North Carolina

Since the proliferation of high-deductible health plans centering the patient in the role of consumer, the US health care system has placed snowballing demands on the patient. Patients are expected to navigate complex bureaucracies and choose from an increasing variety of health insurance options. Consumers frequently face substantial cost-sharing and are expected to differentiate between low-and high-value care.1–3 At the same time, health care delivery mechanisms have become more complex. Medical practitioner—both physicians and hospitals—are vertically integrating at a rapid rate.4,5 Payment is trending toward models that reward health care providers for better care and improved outcomes rather than for volume.6 These two ongoing trends may confuse patients and lead to mistrust as reforms focus on the relationships between clinicians and payers rather than the patient experience.

North Carolina is transitioning its health care delivery and finance model toward value-based care. Blue Cross and Blue Shield of North Carolina has substantially expanded and enhanced a wide number of payment models that strive to move North Carolina toward value-based care while improving quality. NC Medicaid has transformed itself from a fee-for-service, centrally directed care model to a system of distributed, regional care managed by prepaid health plans.7 NC Medicaid is exploring comprehensive care delivery integration through two pilot projects: the state now links some Medicaid beneficiaries with social risk factors to needed social services through the Healthy Opportunities Pilots program,8 and the Integrated Care for Kids model (NC-INCK) seeks to improve care coordination to address the health and developmental needs of children with the intent of reducing long-term social service and medical spending.9 All of these efforts are movements toward preventive, longitudinal, population-based care instead of the treatment of acute episodes on the legacy fee-for-service model.10–12

Today, patients often do not know if their care is fully, partially, or not at all within a transformative value-based model. For instance, the Medicare Shared Savings Program (MSSP), which allows clinical groups to form Accountable Care Organizations (ACO), assigns individuals to an ACO based on prior claims history without notifying a beneficiary.13,14 This invisibility buys bureaucratic simplicity, but it spends social trust.

As North Carolina continues its transition to value-based care, patients will move to progressively more unfamiliar systems. Unfamiliar systems mean unfamiliar incentives. Trust will be a key component of success even as we exist in a time of increased polarization and varying epistemologies that have been highlighted and exacerbated by the COVID-19 pandemic.15

We are woefully uninformed about how to build trust, in large part because the definition of trust is not universal. The Journal of Health Politics, Policy and Law defines trust as “a belief that individuals and institutions will act appropriately and perform competently, responsibly, and in a manner considerate of our interests”.16 Within the context of value-based health care transformation, the realignment of incentives could frequently come into conflict with perceptions of interest and appropriateness. Trustworthiness is therefore difficult to measure or observe fully, even as lack of patient trust can delay care and negatively impact health.17

Trust can be a critical enabler of improved health. A key study found that increased social trust driven by racial concordance between patients and primary care providers substantially increased Black males’ use of preventive care.18 This increase in preventive care takeup could plausibly reduce the Black-White male gap in cardiovascular mortality by 19%.18 Levels of trust between patients and clinicians vary by type of clinician. Nurses, who commonly spend more time building social rapport, are more frequently trusted than physicians.19,20 Nurses have been shown to build trust via reliability by doing what they say they will do, spending time with patients as they wait for procedures or test results, and taking measures to reduce unpleasantness,21,22 for example by administering intravenous medication very slowly so that it hurts less increases children’s trust in the nurse.23

Health care organizations have some systems in place already that are designed to improve quality of care and build trust. These systems include ethics review boards and morbidity and mortality conferences, where all cases resulting in injury or death are discussed on a weekly basis. In the context of care transformation, these differences in trust sourcing need to be recognized and strengthened in both clinician-patient dynamics and patient-organizational contexts.

Value-based care models are fundamentally complex. On top of that, models engage in technocratic tinkering to opaquely shift and realign incentives.24 Opacity and complexity create and construct administrative burdens for patients.25 We encounter administrative burdens when we interact with social services and care.26 Learning burdens can include the time and effort spent identifying which insurer covers a needed drug, while administrative costs could include the requirement to complete forms in non-intuitive manners or seek reimbursement for care provided out of network.

Patients who are expected to act as well-informed consumers are severely underinformed; health and health insurance literacy are low.27,28 Many individuals are unable to define basic terms such as “deductible,” “co-insurance,” or “provider network”.29 Members of historically marginalized groups frequently have especially substantial barriers to effective understanding of health and health insurance.30,31 Additionally, individuals possessing low levels of literacy and numeracy are more likely to be challenged in understanding the complex financial instrumentation of health insurance.32,33

One of the potential challenges that may decrease trust in health insurance and value-based care transformation is the frequent use of medical jargon by health insurers. Complex jargon is further complicated when insurers use slightly different words to describe the same concept. Individuals are first expected to compare a single insurer’s multiple benefit packages against their preferences, which is a complex task in and of itself. Then, individuals are expected to compare multiple insurers, each with their own language for the same concept. This complexity in health insurance terminology is unnecessary, confusing, and incredibly solvable.

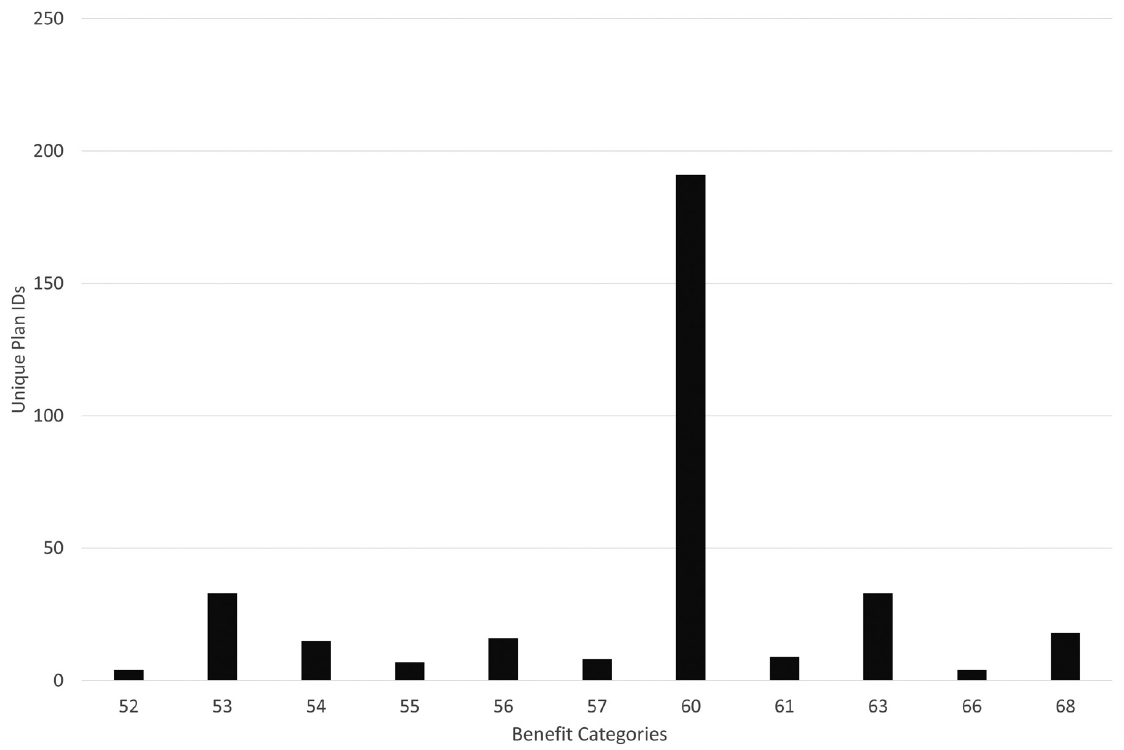

We present a simple example of this unneeded complexity in the 2023 ACA individual health insurance markets in Figure 1. We examined the plans eligible for federal premium subsidies that were sold in North Carolina on Healthcare.gov for coverage during 2023. We extracted this data from the 2023 Benefit and Cost Sharing Public Use File. We excluded from consideration dental-only plans.

Insurers allocate services to benefit categories. We counted benefit-covered categories, such as “primary care services for illness” or “specialty drug.” These categorizations may vary between each insurer, and insurers can offer different numbers of categories between the plans they sell.

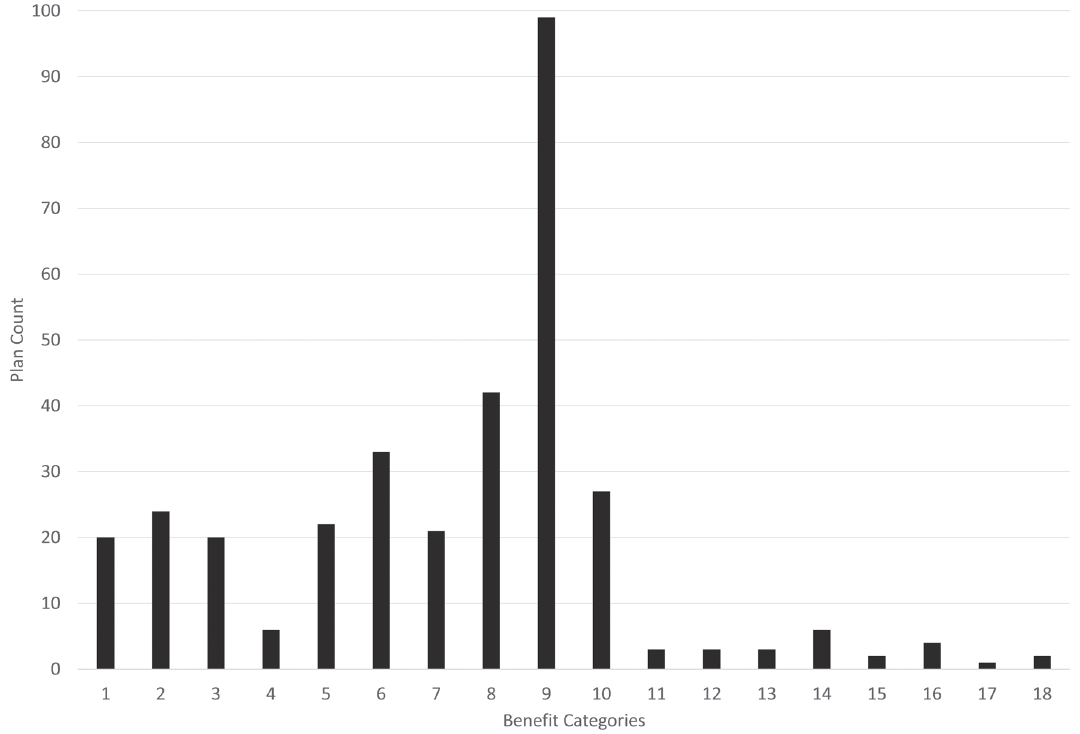

Figure 1 is a bar graph of the different number of health insurance benefit categories offered by each plan in North Carolina. The mean plan has 59.4 (SD 0.19) benefit categories, with a median of 60 and a range from 52 to 68 benefit categories. Once individuals recognize what is covered in each policy, they must interpret how their coverage actually works for sharing costs. Each benefit category has a cost-sharing concept. A benefit can have a combination of deductible (what people pay before the insurer pays anything), coinsurance (a percentage of the final bill), and copay (a per day, stay, or service charge). Some benefits, like flu shots, have absolutely no cost-sharing—they are free to the patient. Other benefits, such as inpatient hospital stays, can have complex cost-sharing. Figure 2 shows the count of unique ACA plans in North Carolina for 2023 by the number of benefit cost-sharing concepts used. The mean plan uses 7.22 (SD 0.18) benefit concepts with a range from 1 to 18 concepts.

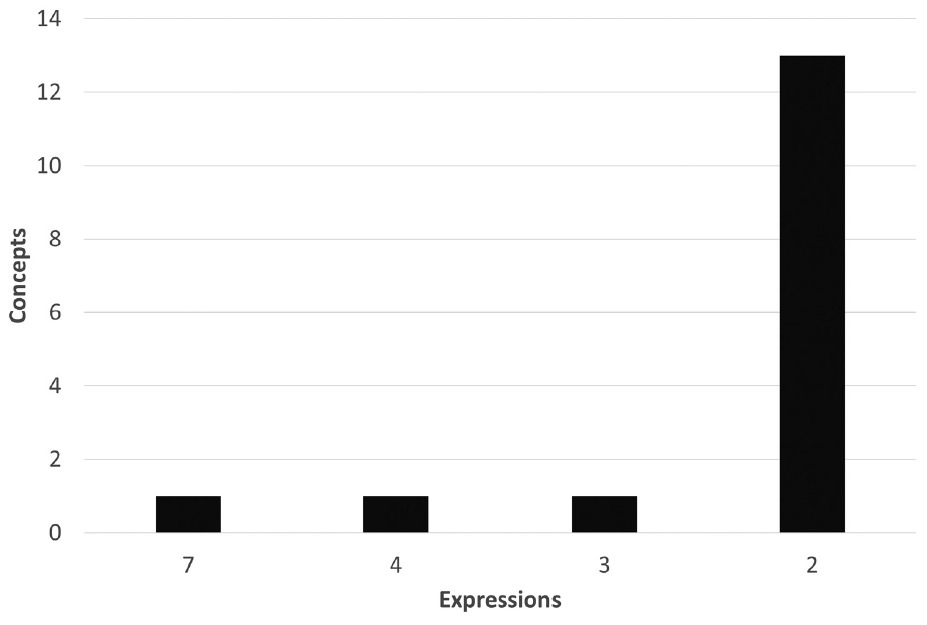

More notably, a benefit concept can be expressed in many ways. Table 1 shows a limited number of ways that the concept of “no charge to the patient” is expressed. As shown in Table 1, insurers can use the same expression for a given benefit concept, or they can use multiple expressions for the same concept. Different insurers are not guaranteed to use the same expression for the same concept. Figure 3 displays the count of expressions of the same concept by the number of benefit categories in North Carolina. We see that the most used benefit concepts have the most expressions. The concept of “no charge to the patient” is communicated in seven unique ways. The second most common concept of “only deductible” is stated four different ways. For individuals operating under uncertainty and limited knowledge, variations in language like these for a single concept could lead to a mistake in plan choice that causes them to face substantial, unwarranted health care costs.

This is just one simple example of needless complexity that may decrease trust. Individuals may credibly believe that complexity is merely a means of confusion designed to transfer money and power to large, bureaucratic entities whose interests are not aligned with the patient and citizen.

Steps Forward

Health care reform and care transformation is an intricate process with new incentives and patterns of care developing constantly. Patients who are exposed to increasing levels of choice need support and assistance, which at the very least includes plain language and clarity from health insurers. Simplifying and standardizing language would be an immediate first step. As lessons that patients learned in fee-for-service models become obsolete, additional assistance, such as access to patient navigators, could minimize confusion.34 Health insurance navigators have been shown to be particularly effective at assisting marginalized and low-income populations.35

Trust can be built and maintained if there are clear pathways to correcting errors and perverse incentives. As clinical groups take on more financial risk, patients may plausibly believe care decisions are being driven by financial self-interest instead of their best interest. Clear forms of appeal and advocacy could limit any belief that care is not being delivered that is in the patient’s best interest. For instance, Connecticut has an Office of the Healthcare Advocate, which is funded to advocate for patients. Nurses, lawyers, and social workers listen and resolve consumer complaints about their care and insurance.

Finally, preexisting sources of trust must be enhanced and leaned into as care is transformed in the state. Current structures, such as hospital mortality and morbidity committees and hospital ethics review boards, strengthen patients’ belief that they are receiving the best care possible. Nurses have historically been able to develop strong rapport, and other clinicians could learn from their example. We can further enhance accessibility and understanding of the care transformation journey by developing common programs that minimize physician confusion and common measure banks that give patients a consistent experience over time. These steps are achievable, well-documented, and will allow for the patient’s experience to be centered in a way that it is not today.

Acknowledgments

The data referenced for Table 1, Figure 2, and Figure 3 are from an ongoing study on the evolution of how insurers use language to describe benefit concepts on Healthcare.gov from 2014 to 2023. Elements of this study have been submitted to peer review in the past and will likely be submitted in the future as we describe the language used to convey benefit information. All data are available upon request to David M. Anderson (dma34@duke.edu). The author has received, in the past three years, consulting fees from Alliant Health Plans, EvenSunLLC, and Silverspread Consulting LLC for Affordable Care Act work unrelated to the topics in this article. Jillian C. Ryan has no disclosures to make.